Menu

Leveraged Products typically aim to deliver a daily return equivalent to a multiple of the underlying index return. For example, if the underlying index rises by 10 per cent on a given day, two times (2x) the Leveraged Product should deliver a 20 per cent return on that day.

At or around the close of trading on the NASDAQ on each Business Day, the Product will seek to rebalance its portfolio, by increasing exposure in response to the Index’s Daily gains or reducing exposure in response to the Index’s Daily losses, so that its Daily leverage exposure ratio to the Index is consistent with the Product’s investment objective.

The table below illustrates how the Product as a leveraged product will rebalance its position following the movement of the Index by the end of the day.* Assuming that the initial Net Asset Value of the Product is 100 on Day 0, the Product will need to have an exposure of 200 to meet the objective of the Product. If the Index increases by 20% during the day, the Net Asset Value of the Product would have increased to 140, making the exposure of the Product 240. As the Product needs an futures exposure of 280, which is 2x the Product’s Net Asset Value at closing, the Product will need to rebalance its position by an additional 40.

Day 1 illustrates the rebalancing requirements if the Index falls by 10% on the subsequent day; Day 2 illustrates the rebalancing requirements if the Index rises by 10% on the subsequent day.

| Calculation | Day 0 | Day 1 | Day 2 | |

| (a) Initial Product NAV | 100.0 | 140.0 | 112.0 | |

| (b) Initial exposure | (b) = (a) x 2 | 200.0 | 280.0 | 224.0 |

| (c) Daily Index change (%) | 20% | -10% | 10% | |

| (d) Profit/loss on exposure | (d) = (b) x (c) | 40.0 | -28.0 | 22.40 |

| (e) Closing Product NAV | (e) = (a) + (d) | 140.0 | 112.0 | 134.40 |

| (f) Closing exposure before rebalancing | (f) = (b) x (1+ (c)) | 240.0 | 252.0 | 246.40 |

| (g) Target exposure to maintain leverage ratio |

(g) = (e) x 2 | 280.0 | 224.0 | 268.80 |

| (h) Required rebalancing amount | (h) = (g) – (f) | 40.0 | -28.0 | 22.40 |

* The above figures are calculated before fees and expenses.

A “roll” occurs when an existing E-mini NASDAQ 100 Future is about to expire and is replaced with an E-mini NASDAQ 100 Future representing the same underlying but with a later expiration date. The Manager has full discretion of futures rolling execution to meet the Product’s investment objective. The rolling of a E-mini NASDAQ 100 Future will occur on a single day within an 8-calendar day period in the last calendar month of each quarter (between 8 calendar days before the last trading day of the nearest quarterly E-mini NASDAQ 100 Futures and one business day before the last trading day of the nearest quarterly E-mini NASDAQ 100 Futures).

The objective of the Product is to provide investment results that, before fees and expenses, closely correspond to twice the performance of the Index on a Daily basis only. Therefore the Product should not be equated with seeking a leveraged position for periods longer than a day. The point-to-point performance of the Product over a period longer than one day may not be twice the performance of the Index over the same period of time due to the effect of “path dependency” and compounding of the Daily returns of the Index.

The performance of the Product before deduction of fees and expenses for periods longer than a single day, especially in periods of market volatility which has a negative impact on the cumulative return of the Product, may not be twice the return of the Index and may be completely uncorrelated to the extent of change of the Index over the same period.

The Product’s objective is to provide returns which are of a predetermined leverage factor (2x) of the Daily performance of the Index. The Product rebalances its portfolio on a Daily basis, increasing exposure in response to the Index’s Daily gains or reducing exposure in response to the Index’s Daily losses. This means that for a period longer than one Business Day, the pursuit of a Daily leveraged investment objective may result in Daily leveraged compounding for the Product. As such, the Product’s performance may not track twice the cumulative Index return over a period greater than 1 Business Day. This means that the return of the Index over a period of time greater than a single day multiplied by 200% generally will not equal the Product’s performance over that same period. Over time, the cumulative percentage increase or decrease in the value of the Product’s portfolio may diverge significantly from the cumulative percentage increase or decrease in of the return of the Index due to the compounding effect of losses and gains on the returns of the Product.

The following scenarios illustrate how the Product’s performance may deviate from that of the cumulative Index return (2x) over a longer period of time in various market conditions. All the scenarios are based on a hypothetical USD10 investment in the Product.

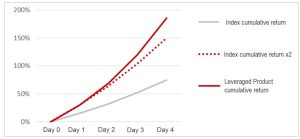

Scenario I: Continuous Upward Trend

In a continuous upward trend, where the Index rises steadily for more than 1 Business Day, the Product’s accumulated return will be greater than twice the cumulative Index gain. As illustrated in the scenario below, where an investor has invested in the Product on day 0 and the Index grows by 15% Daily for 4 Business Days, by day 4 the Product would have an accumulated gain of 185.61%, compared with a 149.80% gain which is twice the cumulative Index return..

| Index Daily return |

Index level |

Index cumulative return | Leveraged Product Daily return |

Leveraged Product NAV | Cumulative performance: Leveraged product | Cumulative performance: 2x of Index |

|

| Day 0 | 100.00 | 0.00% | USD 10.00 | 0.00% | 0.00% | ||

| Day 1 | 15.0% | 115.00 | 15.00% | 30.0% | USD 13.00 | 30.00% | 30.00% |

| Day 2 | 15.0% | 132.25 | 32.25% | 30.0% | USD 16.90 | 69.00% | 64.50% |

| Day 3 | 15.0% | 152.09 | 52.09% | 30.0% | USD 21.97 | 119.70% | 104.18% |

| Day 4 | 15.0% | 174.90 | 74.90% | 30.0% | USD 28.56 | 185.61% | 149.80% |

The chart below further illustrates the difference between (i) the Product’s performance; (ii) twice the cumulative Index return and (iii) cumulative Index return, in a continuous upward market trend over a period greater than 1 Business Day.

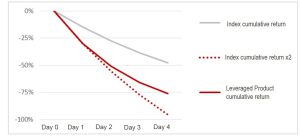

Scenario II: Continuous Downward Trend

In a continuous downward trend, where the Index falls steadily for more than 1 Business Day, the Product’s accumulated loss will be less than twice the cumulative Index loss. As illustrated in the scenario below, where an investor has invested in the Product on day 0 and the Index falls by 15% Daily for 4 Business Days, by day 4 the Product would have an accumulated loss of 75.99%, compared with a 95.60% loss which is twice the cumulative Index return.

| Index Daily return |

Index level |

Index cumulative return | Leveraged Product Daily return |

Leveraged Product NAV | Cumulative performance: Leveraged product | Cumulative performance: 2x of Index |

|

| Day 0 | 100.00 | 0.00% | USD 10.00 | 0.00% | 0.00% | ||

| Day 1 | -15.0% | 85.00 | -15.00% | -30.0% | USD 7.00 | -30.00% | -30.00% |

| Day 2 | -15.0% | 72.25 | -27.75% | -30.0% | USD 4.90 | -51.00% | -55.50% |

| Day 3 | -15.0% | 61.41 | -38.59% | -30.0% | USD 3.43 | -65.70% | -77.18% |

| Day 4 | -15.0% | 52.20 | -47.80% | -30.0% | USD 2.40 | -75.99% | -95.60% |

The chart below further illustrates the difference between (i) the Product’s performance; (ii) twice the cumulative Index return and (iii) cumulative Index return, in a continuous downward market trend over a period greater than 1 Business Day.

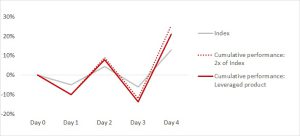

Scenario III: Volatile Upward Trend

In a volatile upward trend, where the Index generally moves upward over a period longer than 1 Business Day but with Daily volatility, the Product’s performance may be adversely affected in that the Product’s performance may fall short of twice the cumulative Index return. As illustrated in the scenario below, where the Index grows by 12.86% over 5 Business Days but with Daily volatility, the Product would have an accumulated gain of 20.96%, compared with a 25.72% gain which is twice the cumulative Index return.

| Index Daily return |

Index level |

Index cumulative return | Leveraged Product Daily return |

Leveraged Product NAV | Cumulative performance: Leveraged product | Cumulative performance: 2x of Index |

|

| Day 0 | 100.00 | 0.00% | USD 10.00 | 0.00% | 0.00% | ||

| Day 1 | -5.0% | 95.00 | -5.00% | -10.0% | USD 9.00 | -10.00% | -10.00% |

| Day 2 | 10.0% | 104.50 | 4.50% | 20.0% | USD 10.80 | 8.00% | 9.00% |

| Day 3 | -10.0% | 94.05 | -5.95% | -20.0% | USD 8.64 | -13.60% | -11.90% |

| Day 4 | 20.0% | 112.86 | 12.86% | 40.0% | USD 12.10 | 20.96% | 25.75% |

The chart below further illustrates the difference between (i) the Product’s performance; (ii) twice the cumulative Index return and (iii) cumulative Index return, in a volatile upward market trend over a period greater than 1 Business Day

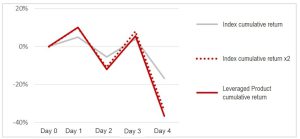

Scenario IV: Volatile Downward Trend

In a volatile downward trend, where the Index generally moves downward over a period longer than 1 Business Day but with Daily volatility, the Product’s performance may be adversely affected in that the Product’s performance may be more than twice the cumulative Index loss. As illustrated in the scenario below, where the Index falls by 16.84% over 5 Business Days but with Daily volatility, the Product would have an accumulated loss of 36.64%, compared with a 33.68% loss which is twice the cumulative Index return.

| Index Daily return |

Index level |

Index cumulative return | Leveraged Product Daily return |

Leveraged Product NAV | Cumulative performance: Leveraged product | Cumulative performance: 2x of Index |

|

| Day 0 | 100.00 | 0.00% | USD 10.00 | 0.00% | 0.00% | ||

| Day 1 | 5.0% | 105.00 | 5.00% | 10.0% | USD 11.00 | 10.00% | 10.00% |

| Day 2 | -10.0% | 94.50 | -5.50% | -20.0% | USD 8.80 | -12.00% | -11.00% |

| Day 3 | 10.0% | 103.95 | 3.95% | 20.0% | USD 10.56 | 5.60% | 7.90% |

| Day 4 | -20.0% | 83.16 | -16.84% | -40.0% | USD 6.34 | -36.64% | -33.68% |

The chart below further illustrates the difference between (i) the Product’s performance; (ii) twice the cumulative Index return and (iii) cumulative Index return, in a volatile downward market trend over a period greater than 1 Business Day.

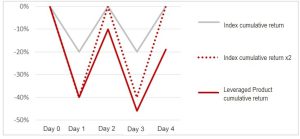

Scenario V: Volatile Market with Flat Index Performance

In a volatile market with flat index performance, the aforementioned compounding can have an adverse effect on the performance of the Product. As illustrated below, even if the Index has returned to its previous level, the Product may lose value.

| Index Daily return |

Index level |

Index cumulative return | Leveraged Product Daily return |

Leveraged Product NAV | Cumulative performance: Leveraged product | Cumulative performance: 2x of Index |

|

| Day 0 | 100.00 | 0.00% | USD 10.00 | 0.00% | 0.00% | ||

| Day 1 | -20.0% | 80.00 | -20.00% | -40.0% | USD 6.00 | -40.00% | -40.00% |

| Day 2 | 25.0% | 100.50 | 0.00% | 50.0% | USD 9.00 | -10.00% | 0.00% |

| Day 3 | -20.0% | 80.00 | -20.00% | -40.0% | USD 5.40 | -46.00% | -40.00% |

| Day 4 | 25.0% | 100.00 | 0.00% | 50.0% | USD 8.10 | -19.00% | 0.00% |

The chart below further illustrates the difference between (i) the Product’s performance; (ii) twice the cumulative Index return and (iii) cumulative Index return, in a volatile market with flat index performance over a period greater than 1 Business Day.

As illustrated in the graphs and the tables, the cumulative performance of the Product before deduction of fees and expenses is not equal to twice the cumulative performance of the Index over a period longer than 1 Business Day.

For further illustration of the Product’s performance under different market conditions, investors may access the ‘performance simulator’ on the Product’s website at http://liproduct.chinaamc.com.hk/HKen/7261, which will show the Product’s historical performance data during a selected time period since the launch of the Product.

The maximum potential loss when buying leveraged and inverse Products is the entire value of the initial investment. However, the maximum potential loss when investors trade futures could be greater than the initial collateral posted which would result in additional margin calls.